What are 4 steps to personal finance planning?

Step 4. Develop a Comprehensive Financial Plan. Proceeding forward, the subsequent step in the financial planning process entails crafting a comprehensive financial plan. This plan should encompass a wide spectrum of both short-term and long-term goals and objectives.

Step 4. Develop a Comprehensive Financial Plan. Proceeding forward, the subsequent step in the financial planning process entails crafting a comprehensive financial plan. This plan should encompass a wide spectrum of both short-term and long-term goals and objectives.

By taking the time to save and invest, you can ensure a more stable future for yourself and your loved ones. Let's take a look at some key financial planning tips for four different life stages: early career, mid-career, pre-retirement, and early retirement.

The four main types of financial planning are cash flow planning, tax planning, investment planning, and retirement planning. Each of these types of financial planning has different goals, concerns, and objectives.

The main elements of a financial plan include a retirement strategy, a risk management plan, a long-term investment plan, a tax reduction strategy, and an estate plan.

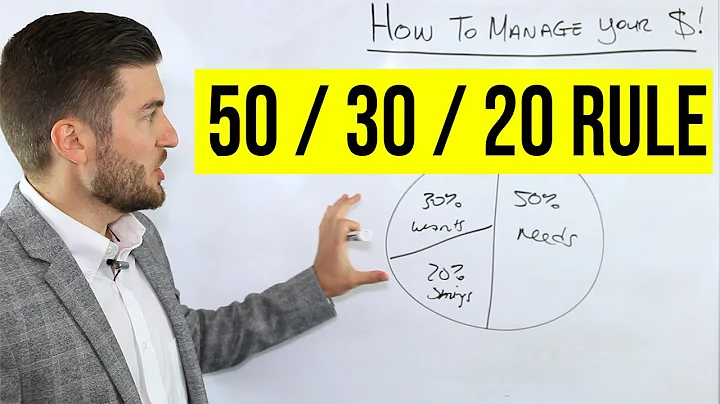

- Step 1: Know Your Numbers. Comparing your income to monthly payments will help you budget for savings. ...

- Step 2: Protect What's Yours. Insurance is the best defense against the unexpected. ...

- Step 3: Fund Your Future. How do you see your retirement? ...

- Step 4: Build Your Wealth.

There are six steps in the financial planning process: understanding your financial circ*mstances, identifying goals, analyzing your current course of action, developing a financial plan, and monitoring progress and updating. This is a great question to ask if you're considering working with a financial planner.

There are four main areas of finance: banks, institutions, public accounting and corporate. Courses within the finance major provide a solid background in many subjects including: Financial markets and intermediaries.

- Step 1: Assess your financial foothold. ...

- Step 2: Define your financial goals. ...

- Step 3: Research financial strategies. ...

- Step 4: Put your financial plan into action. ...

- Step 5: Monitor and evolve your financial plan.

There are six steps in personal finance planning: EGADIM: Establish financial goal; Gather data; Analyze data; Develop a plan; Implement the plan; Monitor the plan. Establishing the goal is the first step.

What are the 4 types of financial management explain?

Most financial management plans will break them down into four elements commonly recognised in financial management. These four elements are planning, controlling, organising & directing, and decision making. With a structure and plan that follows this, a business may find that it isn't as overwhelming as it seems.

Barbara Stanny describes the four stages of wealth as Survival, Stability, Wealth, and Affluence. Based on thousands of hours as both a client and a counselor in the money coaching process, here is my understanding of each stage.

- Financial Planning and Forecasting. ...

- Cash Management. ...

- Cash flow forecasting. ...

- Estimating Capital Expenses. ...

- Determining Capital Structure. ...

- Choosing Sources of Funds. ...

- Procurement of Funds. ...

- Investment of Funds.

- Establish Goals.

- Assess Risk.

- Analyze Cash Flow.

- Protect Your Assets.

- Evaluate Your Investment Strategy.

- Consider Estate Planning.

- Implement and Monitor Your Decisions.

- AWM&T: Your Choice for Financial Fitness.

- Setting financial goals. ...

- Net worth statement. ...

- Budget and cash flow planning. ...

- Debt management plan. ...

- Retirement plan. ...

- Emergency funds. ...

- Insurance coverage. ...

- Estate plan.

Financial planning is the process of taking a comprehensive look at your financial situation and building a specific financial plan to reach your goals. As a result, financial planning often delves into multiple areas of finance, including investing, taxes, savings, retirement, your estate, insurance and more.

- Set financial goals. It's good to have a clear idea of why you're saving your hard-earned money. ...

- Plan for taxes. It can go a long way toward helping you keep more of your money. ...

- Manage debt. ...

- Plan for retirement. ...

- Create an estate plan.

There are six stages to develop a financial plan and to carry out personal money management. From beginning to end, a certified financial planner professional guides you through the financial planning process - keeping in view your current financial situation and economic background.

Making a budget is the single most useful thing you can do to take control of your money. It helps you see where your money is going, makes it easier to pay bills on time, save money for the things you want, prepare for emergencies and plan for the future.

Get started on path to financial success with these three steps: determining budgets, tracking spending, and creating realistic savings goals.

What are the three most common reasons firms fail financially?

In conclusion, the three most common reasons for financial failure are lack of financial planning, ineffective cost management, and insufficient market research. Firms that proactively address these issues increase their chances of achieving and maintaining financial stability.

365 Financial Analyst

In the vast landscape of accounting and professional services, the Big 4 – KPMG, EY, PwC, and Deloitte – reign supreme. These titans not only dominate the field in client network and revenue globally but also audit around 80% of public companies in the United States.

What Are the Five Areas of Personal Finance? Though there are several aspects to personal finance, they easily fit into one of five categories: income, spending, savings, investing and protection. These five areas are critical to shaping your personal financial planning.

The most common types of financial institutions include banks, credit unions, insurance companies, and investment companies. These entities offer various products and services for individual and commercial clients, such as deposits, loans, investments, and currency exchange.

1. Assess your financial situation and typical expenses. An important first step is to take stock of your current financial situation. Even if you're not where you'd like to be, be honest with yourself about the income you're currently generating, savings you've accumulated and your general spending habits.